One cannot assess the present state of the Costa del Sol property market and look to the near future without using the perspective that the past couple of years provide. In this sense a clear divide exists between the pre- and post-Covid periods, the latter marked by a sudden rush of demand that has made the past five years among the top-performing in the history of the Costa del Sol.

This is as true of the tourist sector as it is of the real estate market, and as we look back at the past five years, we can summarise the following:

One of the greatest property booms ever on the Costa del Sol

A top-down market dominated by the luxury segment

The ability of the market to absorb high-paced price increases

Premium prices paid for top locations such as the Golden Mile and La Zagaleta

A high degree of off-plan buying, especially in smaller boutique developments

The spread of most new development to Estepona, Benahavis, Fuengirola and Mijas

The rise of Estepona as a prominent property destination in its own right

Post-Brexit diversification of the market, with Scandinavia, the Benelux and Eastern Europe driving growth but also the continued presence of traditional British and Middle Eastern markets as well as the resurgence of the North American market

In other words, the Costa del Sol property market has been buoyant over the past five years and primarily focused on the luxury segment, with a high concentration of new-built properties contributing to the rise of areas such as Estepona. The question is, will this momentum be maintained into 2026 or will we see a market adjustment with lower transaction volumes and a slowdown in price increases? Which of these circumstances would be better for the medium-term health of the local economy, and what are the internal and external factors that will be helping to shape market conditions in 2026?

Spain

2025 Review

The real estate sector in Spain is characterised by two distinct parts - the national Spanish market and that of the ‘Costas’ (coastal areas), where the former is dominated by domestic primary homebuyers and the second mostly by foreign buyers of holiday homes. The statistics reveal this much and sometimes they can paint two very distinct pictures, though at the present moment the divergence is not so great. That said, the Costas - and for the purposes of this study we will focus on the Costa del Sol - tend to move ahead of the rest of the country as they are more finely tuned to international market trends.

National market performance

The Spanish property market can look back on a strong year in which both sales and prices continued to grow, though as always, the trend is highly diverse depending on the region and the urban/rural divide, with the likes of Madrid, Barcelona, Valencia, Bilbao and especially San Sebastian topping the list.

Domestic demand has recently even outpaced that of foreign buyers, with the latter dropping from an overall market share of 14,10% in Q2 2025 to 13,52% in Q4 2025. This strong showing is the result of the fact that Spain has been one of the top performers in Europe since the end of the Covid pandemic, averaging between 2%- 3% economic growth during this period. The jobs and average increase in wages produced by this is enabling a growing number of Spanish people to purchase homes in spite of price increases, and in the process, promoting renewed investment in the construction of homes.

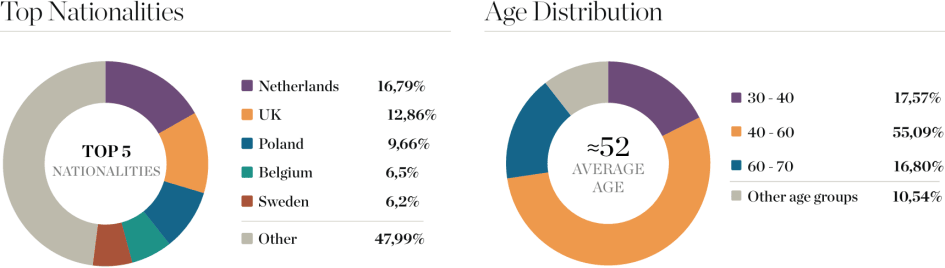

Statistics Roundup 2025

Top 10 Nationalities

Andalusia

Regional market dynamics

As a region, Andalusia leads Spain in sales growth, driven by a combination of strong domestic and foreign buyer demand, with dynamic price evolution to match. As in the rest of the country, the bulk of this activity is concentrated in the cities and coastal areas, especially Málaga and the Costa del Sol, the motors of the regional market.

Statistics Roundup 2025

Top 10 Nationalities

Golden Triangle

Price evolution across the core markets

The below graph shows that the increase in the average price of properties sold has slowed down in Marbella and Estepona. Benahavis is the exception, and its more rapid recent price increases push up the average for the Golden Triangle. On the whole, however, the trend is towards a gradual slowing down in the rate of price increases.

Price growth levels off

Q1 2026 data shows mixed movements in average prices across the different municipalities compared to Q4 2025. Marbella recorded a 4.7% increase and Benahavis remained broadly stablem sith a 0.7% ride, whole Estepona fell by 6.9% after the strong increase recorded at the end of 2025. Overall, the Golden Triangle average remained unchanged compared with Q4 2025, at 4,322 €/m2, This points to short-term stabilisation in average prices.

Source: Portal Estadístico Notariado

Marbella

A mature and supply-constrained market

As the official jewel in the crown of the Costa del Sol, Marbella continues to be very popular among HNW buyers, particularly in areas where limited availability blends with a great deal of desirability to produce record prices (per m2). This applies to top addresses such as Sierra Blanca, Los Monteros, Nueva Andalucía, Puerto Banús and The Golden Mile, on whose beachfront prices of €30.000/m2 have been achieved over the past two years.

Marbella suffers from a limited supply of new homes due to a combination of scarce building land and the well-known urban planning issues (a new planning directive is now more than ten years in the waiting), resulting in a market dominated by resales and renovation properties. The high average price paid by what is predominantly a Northern European market reflects the fact that this is a market with a broad range – from lower prices starting at €300.000 to ultra-luxurious homes of €20 million or more, helping to produce an average price per property in Marbella of €736.866. 2025 saw prices continue to rise, though at a lesser rate than in 2024 and 2023.

Statistics Roundup 2025

Benahavís

A high-value luxury enclave

Though it contains high-profile country clubs and residential areas such as La Zagaleta, El Madroñal, La Quinta, Los Arqueros and Los Flamingos, the Benahavis property market operates on a somewhat smaller scale than those of Marbella and Estepona. It is a predominantly luxury market with a high average purchase price and price per square metre dominated by Northern European buyers and characterised by a high proportion of villas and resale homes. The rate of property value increases is recently outpacing that of Marbella and Estepona, with a number of luxurious projects about to be launched that could further add to this.

Statistics Roundup 2025

Estepona

Expansion driven by new development

Thanks to its available building land and smoother urban planning process, Estepona has had the most dynamic property market on the Costa del Sol in recent years, with a large proportion of new homes built in the region. This has helped to really put it on the map as a prime destination in its own right, with prices per square metre that are catching up with Marbella yet an average price per property that is still well below that of Benahavis and Marbella.

The new-built homes here are particularly popular among Polish, Dutch and Belgian buyers, with Estepona also marked by a relatively high proportion of domestic buyers and apartments within the property mix. New projects continue to be launched and price growth remains solid, as Estepona continues to catch up with Marbella.

Statistics Roundup 2025

Sales across the Golden Triangle - Market share

Total transactions in 2025

Sales evolution. 10-year transaction trends

Source: Portal Estadístico Notariado

Average time a property was on the market. Back to a slower pace

Source: DM Properties

Real selling prices

Micro-location value in Marbella

Real average sales prices across villas, townhouse and apartments (2025).

Real selling prices, as provided by the Notary Statistics Portal (P.E Notariado), represent a new statistic that adds a greater level of practical, non-theoretical information.

The figures are very similar to the official ones released by the property registry offices yet now also provide a breakdown within different parts of major municipalities.

In the case of municipality of Marbella, it is clear that San Pedro and Marbella town - which contain a prominent domestic market - represent the lower end of the statistics, accompanied by Marbella East, an area popular with foreign buyers but where (relatively) abundant land and (relative) distance from Marbella’s core have contributed to lower prices per square metre. This means that you get more house for your money in East Marbella areas such as Santa Clara, El Rosario and Elviria, which also explains why this is one of the key residential areas on the Costa del Sol with a great deal of future potential.

Nueva Andalucía is a somewhat mature area that has already realised much of this potential over the past decade and a half and now offers above all a prime address. It can be seen that Sierra Blanca and Puerto Banús, the prime areas within Marbella for which official data exists, represent the top of the regional market with square metre values of almost €5.500.

Benahavís & Estepona prices

Understanding price dynamics across municipalities

Benahavís

(* according to our own data)

The average price of properties sold within the municipality of Benahavis reflects both its smaller scale (more easily distorted statistics) and the fact that it contains some of the most exclusive residential areas in the region, including country clubs such as La Zagaleta and El Madroñal. That said, the properties here are large and they stand on sizeable plots, which suppresses the average price per m2 when compared with more densely built-up areas such as Puerto Banús, Nueva Andalucía and Sierra Blanca.

Benahavis still has land to develop, a town hall that is business friendly and has created a well-functioning urban planning system, and it will remain a prominent part of the Golden Triangle in spite of the fact that it has no shoreline frontage.

Unfortunately the PE Notariado doesn’t break down prices per m2 by residential area and on the contrary gives a figure for the whole of the municipality and property types (except plots). Based on our own sales within the last 12 months in La Zagaleta where we have been quite active, the average sales price of villas sold has been 6885€/m2. This shows that obviously there can be quite a substantial difference between the municipality average and a specific residential area.

Estepona

Property values have risen considerably in Estepona over the past decade or so, driven by high demand for the modern and increasingly upmarket new villa and apartment projects that have arisen and continue to be built within its municipal confines. This has allowed the town to reduce the gap with Marbella in terms of desirability and price/m2, though there is still some way to go.

The breakdown of areas shows that Estepona’s growth has thus far been focused upon the New Golden Mile, which extends eastwards towards San Pedro (Marbella municipality). Here, square metre prices approach the lower values for Benahavis and Marbella, yet on the westside of Estepona they remain well below this level and closer to traditionally ‘less fashionable’ areas such as Fuengirola, Mijas and Istán. However, as is the case with Marbella East, the western part of Estepona provides the building land and price/value potential as well as an increasing number of new, more upmarket developments that mark it out as a zone with great potential in the near to mid-term.

Price evolution - A decade of change across key markets

Marbella Price Evolution

Marbella’s property market began its post-Financial Crisis recovery well ahead of the rest of the country. It was also the first part of the Costa del Sol to rebound, registering solid growth in sales and prices that peaked in 2018, before slowing down and even flatlining in 2019 and 2020 respectively.

The following year saw a wave of demand put pressure on prices, a process that has continued right up to the present, though the lower rate of price increases could indicate the beginning of a slowing trend.

Benahavís Price Evolution

Benahavis took a little longer to revive than Marbella, still registering a decline in prices in 2015, yet the recovery consolidated the following year, resulting in a phenomenal 31,32% increase in 2018 that was followed by an equally surprising 12,53% drop in average sales prices in 2019. However, in a town with a smaller statistical sample of sales such figures can be easily magnified and/or distorted by the release or selling out of even a single sizeable complex.

Growth was impressive in 2020, continued in 2021 and 2022, and picked up again strongly the following year. 2024 posted a more sober increase in values, which in the end proved to be a singular event as 2025 once again saw an acceleration in property values of almost 10%.

Estepona Price Evolution

Estepona would normally have lagged behind Marbella in terms of recovery but enjoyed its own momentum when the current mayor, José M. García Urbano, began a process of urban renewal that sparked a renaissance of the town and laid the foundations for its newfound popularity as a major destination in its own right.

This much was evident in 2015 from the sharp increase in property prices, driven in large part by new upmarket projects in and around the town. Though 2016 and 2017 saw a drop in values, the market rebounded strongly in 2018 (+29.68%) and 2019 (+15.30%). The Covid year, 2020, witnessed a significant drop that was again followed by impressive levels of property price increases that have continued up to the present moment, albeit at a slower pace.

Golden Triangle price growth and market reality

The Golden Triangle has seen a clear rise in average selling prices over the past decade, with Marbella, Estepona and Benahavís each following their own pace of growth.

Source: Portal Estadístico Notariado

By comparing long-term price evolution with the gap between asking prices and final selling prices in 2025, the data shows a more complete picture of the market. Prices remain strong, but the difference between what sellers ask and what buyers finally pay also points to a more selective market, where pricing accuracy matters more.

Market Gap - Asking prices vs real transactions

% Difference between asking price & final selling price in 2025

Source: DM Properties

What 1 Million € Gets You

Comparative values in the Golden Triangle (Marbella, Estepona, Benahavís). How many square metres of prime property does 1.000.000€ buy you in:

Source: DM Properties|Knight Frank - Date: December 2025. (M): Marbella - (B): Benahavís - (E): Estepona

Team insights

Market feedback and buyer behaviour

Pia Arrieta - Principal Partner

Market & Prices

“Having had a very good year in 2024, we expected 2025 to perhaps be a little slower but in reality it turned out to be one of our best years to date, with strong demand for villas in particular. The market therefore continued to be strong, with people asking for the kind of properties and areas that offer the classic Marbella lifestyle of proximity to beaches, golf courses, nature and quality services. One thing we have noticed is a certain degree of resistance emerging towards the increasing prices of properties. This is particularly so in the mid to higher segment of the market, where some buyers are beginning to reach the level where they either can’t afford to pay more or are not willing to. Interestingly, this is not the case in the upper segment.”

Mariano Beristain - Managing Partner

Areas & Properties

“Although there was also strong demand for apartments and penthouses, villas continue to be very popular, ranging from more compact modern ones to larger properties with spacious private living areas, leisure amenities and well-established gardens. The areas that are very much in demand are the Golden Mile – though supply is limited – Nueva Andalucía, Sierra Blanca, Los Monteros, Guadalmina, La Quinta and its new extension Real de La Quinta, as well as La Zagaleta and El Madroñal, which is experiencing a revival. This is also true of other classic suburbs such as El Paraíso, which is very popular among buyers and investors keen to renovate villas.”

Beatriz Martínez - Marketing Manager

Customer Preferences

“There has been no sudden dramatic change in buyer preferences, but rather a continued evolution of trends that have been an influence over the past few years. These include a desire for space and privacy that followed Covid, the ability to work from home or be close to coworking spaces as there are many digital nomads and people running their businesses from here now, more fulltime living facilities such as storage space, and an evolution of entertainment spaces into single rooms that include home cinema facilities, pool tables, bars, etc. There is also a growing focus on energy efficiency and environmental sustainability, as well as homes that provide a sense of wellbeing.”

Mar Poza - Research & Marketing Manager

Buyer profile

“There has been much said about the average buying age dropping, and while this is true it has perhaps been exaggerated a bit as most of our clients continue to be in the 40 to 60 age range. Most are successful professionals and business owners from what seems to be a widening range of countries that includes traditional markets such as Northern Europe and also a growing number of buyers from countries like Poland and regions such as the Middle East and Ukraine.”

Land & opportunities

Price evolution and development hotspots

Development and Investment

One of the elements often overlooked in market analyses is that of property development and investment – both of which play a vital role in the local sector. In this edition of the DM Properties-Knight Frank Market Report we take a closer look at the characteristics of this segment and the dynamics that drive it.

Land and Price Evolution

Property development is all about land, so the availability of the right kind of plots at prices that allow for the design, construction and commercialisation of real estate projects is the key consideration for developers. Together with finance, it is one of two core resources they require to make projects viable, and apart from the fact that land prices have risen considerably (often outstripping property itself), profit margins also came under pressure from rapidly rising construction costs in the years following the Covid Pandemic, though they appear to have levelled off now.

Add the further complications of Marbella’s urban planning limbo and it becomes clear that life is not always easy for property developers, yet this doesn’t seem to have lessened the interest of investors in this region – no doubt aided by the fact that so far, the sector has been able to pass its rising costs on to the end buyer, with a market that has been remarkably capable of absorbing rapidly rising prices without any significant impact on demand. Meanwhile, the planning issues and limited availability of building land in Marbella have driven most developers to municipalities such as Mijas, Fuengirola, Benahavis and especially Estepona, which has become the focus of much of the new development on this coast over the past decade or so.

Obvious factors that affect land price are the attractiveness of the location, views, proximity and a beachfront setting.

Marbella

€800-€2500/m2 for building plots and development land (typical price above €1000- €1500/m2).

€2500-€5000/m2 for prime areas such as the Golden Mile, Sierra Blanca & beachfront Land scarcity pushes prices up in the main Marbella areas.

Benahavis

€600-€2000/m2 for urbanisations such as Los Flamingos, Los Arqueros and El Madroñal.

€2000-€4000/m2 for prime areas such as La Zagaleta.

The relative availability as well as the hilly topography, distances and lack of beachfront locations lower prices in spite of the presence of exclusive residential areas and country clubs.

Estepona

€400-€1200/m2 in most areas but rising in locations closer to town and beachfront settings.

Land is more readily available in Estepona and generally located in gently undulating terrain not far from the sea, yet for a long time the town was regarded as less fashionable, which suppressed prices. This trend has been reversed and land prices are rising rapidly.

Top areas for property development

The cheapest land is not always the most profitable, so choosing the right spot is all about location and knowing which areas are the most in demand and which command the best prices from homebuyers. For developers, the ideal combination is an up-and-coming residential address that offers capital growth potential for builder and buyer alike. In other words, an area where (land) prices are still attractive but whose increasingly fashionable status favours a good rate of sales, and at rising prices.

Good examples of such areas for both the new construction and home renovation segments originally included Nueva Andalucía, then Nagüeles, Nueva Alcántara and Real de La Quinta before continuing on to the New Golden Mile, Los Flamingos, La Alquería and now also El Paraíso and Bel Air.

Economic context

Growth, risks and global environment

Looking ahead

Having analysed the national, regional and local property market segments in depth and their performance over 2025 relative to previous years, the next step is to preview the coming year, and for this we need to take both local, national and international factors into account.

2025

In summary, 2025 was a good year for the property sector on the Costa del Sol, with continued growth in sales and prices, albeit at a slightly slowing rate. This is not surprising given that it was always clear that maintaining such very high levels would be difficult. In addition, a gentle slowing of pace will also avoid overheating of the market and maintain the conditions for continued growth.

The economic environment

Spain has been one of the top performers within Europe over the past few years and this continued in 2025, when its economy grew by almost 3%. One of the results of this is job creation, with unemployment falling below 10% (with a record 22 million people in employment) and inflation set around an official figure of 2,5%.

Spain’s economy therefore grew almost twice as much as the EU average of 1,4%, with unemployment falling more rapidly (though still higher) and inflation at roughly the same level. Spain is therefore one of the stars of the Eurozone, yet it is not all plain sailing.

The main drivers of growth are:

Foreign investment, for instance in real estate assets and property development.

Tourism, accounting for over 20% of GDP.

EU Investment and Recovery Funds, of which Spain has been a major recipient.

Strong domestic consumer performance driven by high employment, rising wages and population growth – including strong rebounding demand for housing.

4% growth in the construction sector.

Strong service export growth.

Challenges and risks:

Bureaucracy, high taxes, an oversized public sector apparatus and relatively low productivity levels resulting in high costs relative to output challenge growth.

Housing supply and affordability exacerbated by rapid population growth make it difficult to attract labour to urban and coastal growth areas.

Energy price volatility, housing costs and wage growth (outperforming productivity) could push inflation upwards.

Geopolitical environment

Many speak of the global political environment as being unstable but 1) when has it not been so, and 2) for this reason global economies and markets have learned to absorb the shocks and surprises with growing agility.

That said, the sudden eruption of war over Iran and its spilling over into much of the Middle East did come as a surprise to much of the world and has certainly been felt in terms of rapidly rising fuel prices and volatile stock markets. Global growth forecasts for 2026 have already been revised downwards, largely due to the impact of the Middle East conflict on energy prices, inflation and market confidence. The scale of the effect will depend on the duration of the conflict, the speed at which energy supply routes normalise and whether financial markets continue to absorb the shock without a deeper correction. While the baseline outlook still points to growth rather than recession, downside risks remain.

It comes against a European background of growing trade wars, political instability, growing public dissatisfaction and concerns about the rapidly rising cost of living, crime and security. However, such conditions have tended to benefit the Costa del Sol as a beacon of security and quality of life, and this could boost growth once again.

2026 Forecast

A transition towards balance

Economic forecasts for 2026

The Spanish economy is forecast to continue its growth, albeit at a slightly reduced rate of 2-2,5%, with inflation expected to drop to just above 2% and unemployment to fall a little further below 10%. By comparison, the average growth rate of the EU is set at around 1%, with inflation at around the same mark as in Spain and job growth to continue.

The Spanish economy will continue to be driven by the same factors, but the impact of the European and international issues described above combined with pricing concerns could provide challenges. However, the expected lowering of interest rates by the ECB in the course of 2026 should stimulate growth and investment flows.

2026 Forecast and challenges

Early local data for 2026 confirms a more selective market across the Golden Triangle. Sales fell by 35.6% in Q1 2026 compared with Q4 2025, following a strong final quarter of the year. However, average prices held broadly stable over the same period, suggesting that the market is slowing in transaction volume rather than undergoing a broad price correction.

This suggests a gradual return to more balanced market conditions after several highly active years. Demand remains solid, especially for prime and distinctive homes in areas where quality supply is limited. These properties are expected to show the strongest price resilience.

Beyond the most sought-after locations, however, buyers are becoming less willing to accept excessive prices. More frequent asking-price adjustments point to a more disciplined market, where correct pricing will become increasingly important and average selling times are likely to increase.

That said, there continues to be a lack of certain types of homes relative to strong demand:

New apartments on the Golden Mile.

New contemporary villas in Sierra Blanca and Cascada de Camoján.

New built villas in La Zagaleta in the €10-€15 million bracket.

Refurbished or new villas for under €3 million in good (though not necessarily prime) areas.

Refurbished townhouses under €2 million on the Golden Mile.

We have also noticed a lower number of ‘flipping’ opportunities in prime or good areas, a sign that they are maturing in terms of their growth cycle. This opens the door to new, as yet unconsolidated areas where land is still available. Developers and buyers alike increasingly look to such zones when there are indications that they have good growth and price increase potential. The suburbs that currently qualify as such are Bel Air, El Paraíso, Estepona and Real de La Quinta. Elsewhere, it is becoming increasingly challenging to transfer the prevailing high prices to buyers as the market appears to be becoming less capable of absorbing them.

Additionally, as of January 2026, the tax advantage available to properties bought for intended resale purposes has changed, as the previously applicable reduction from 7% to 2% transfer tax now only applies to properties under €500.000, while the resale period has been reduced from 5 to 2 years.

Marbella’s continued growth also brings practical challenges. Road mobility remains an issue along the A-7/AP-7 corridor and in busy areas such as San Pedro Alcántara, Puerto Banús and East Marbella at peak times. Future development will also depend on water, electricity and transport infrastructure keeping pace. The recovery of the Marbella desalination plant is positive, but continued investment will be essential to support resident demand, tourism and new development sustainably.

Urban planning in Marbella

Towards greater legal certainty

Urban planning has been a complex aspect of Marbella’s property market for decades. The municipality still uses the 1986 General Plan as its planning base, a document designed for a different city. Since then, Marbella has grown in population, economic activity, services, residential tourism and international demand. This gap between the current framework and the city’s reality has created uncertainty, but also shown Marbella’s strength as a residential and investment destination.

The situation became more complex after several failed attempts to update the planning framework. The 1998 plan never came fully into force, although licences were granted under it. This left thousands of homes in an irregular planning situation. The 2010 General Plan then attempted to normalise the situation, but it was annulled by the Supreme Court in 2015. Marbella returned to the 1986 framework.

In this context, the new Plan General de Ordenación Municipal, or PGOM, represents an important step forward. It is being processed under Andalusia’s LISTA law, which separates municipal planning into two instruments. The PGOM defines the general model for the city, including land classification, major infrastructure, mobility, green areas, environmental protection and future growth areas. The POU will develop detailed rules for urban land, covering uses, heights, building parameters and conditions for specific plots and neighbourhoods.

What the new planning framework brings

Greater legal certainty.

Clearer land classification.

Land reserved for future infrastructure.

Greater focus on sustainability and mobility.

A more structured integration of inherited planning situations.

Detailed rules through the future POU.

Recent progress on the PGOM

Since 2024, the PGOM has made significant progress. In June 2025, Marbella Town Hall approved the final proposal. The key milestone came in February 2026, when the Junta de Andalucía issued a favourable report on the final document. This allows the Town Hall to take the PGOM to the Plenary for final approval during 2026. The POU is expected to continue its processing, with initial approval anticipated in 2026 and final approval estimated between 2027 and 2028.

According to municipal information, the document classifies around 53 million square metres as urban land and identifies around 64 million square metres as rural land, of which approximately 30 million square metres could be subject to transformation. This should not be read as an immediate release of land for development. Future development will depend on specific procedures, technical viability, environmental requirements, infrastructure capacity and further approvals.

Inherited planning situations

One sensitive challenge is the integration of homes left in an irregular planning situation after the issues linked to the 1998 plan and the annulment of the 2010 General Plan. The PGOM does not provide automatic regularisation. Its role is to create a more solid framework to organise the real city and integrate, where legally possible, inherited situations that have formed part of Marbella’s urban fabric for many years.

A new model for the city

The new planning framework is not only a way to allow further development. Its purpose is to organise Marbella more effectively and plan its future with clearer criteria. The proposed model reinforces several concepts:

Greener, with more open space.

Garden-city, with low density as a key value.

Polycentric, beyond Marbella and San Pedro.

Better connected, with stronger mobility links.

Aligned with residential tourism and local demand.

For the property market, the main value of the PGOM lies in predictability. A more modern framework can strengthen confidence among buyers, owners, developers and investors. It can also improve transparency and support more orderly planning for new residential areas, public facilities and infrastructure.

Marbella is therefore moving from uncertainty towards a more structured model. In a market where location, scarcity and legal certainty are key factors, this change represents a significant step for the future of the city.

Global context

Marbella within the international prime market

Marbella in the Global Context

The Costa del Sol, and Marbella in particular, continues to strengthen its position as one of the world’s leading prime residential markets. While official data from the Spanish Notaries indicates average price growth of 7.86% in Marbella in 2025 across all market segments, the prime residential sector outperformed this trend. According to The Wealth Report 2026 by Knight Frank, prime residential prices in Marbella increased by 8.1%, reflecting continued demand for high-quality assets in top locations.

This placed Marbella among the world’s top-performing luxury residential markets and firmly within the top tier of the Prime International Residential Index (PIRI 100). This performance is particularly significant in a broader global context: while prime residential prices rose by an average of 3.2% worldwide in 2025, Marbella outpaced that figure comfortably, reinforcing its appeal as a high-demand, supply-constrained market.

A global lifestyle and capital destination

Marbella is no longer simply a regional or European market. It has evolved into a global destination for internationally mobile wealth.

Across Europe, demand for prime residential property is increasingly driven by buyers seeking stability, quality of life and long-term asset security. Within this landscape, lifestyle markets - including Marbella - continue to attract strong and sustained capital inflows.

This positions the Costa del Sol alongside other established second-home and lifestyle destinations such as the Alps and key Mediterranean locations, but with a broader and more diversified international buyer base.

The role of safe-haven demand

In an environment defined by geopolitical uncertainty, inflationary pressures and shifting tax regimes, prime residential markets that combine lifestyle appeal with political and economic stability are attracting increasing attention.

Marbella benefits directly from this trend. Its combination of climate, infrastructure, accessibility and established international community makes it an attractive option for buyers seeking both lifestyle and capital preservation. As a result, the market continues to absorb demand not only from traditional European buyers, but also from North America, the Middle East and emerging wealth markets.

Evolving buyer motivations

A notable shift in global prime markets is the growing importance of long-term, lifestyle-driven ownership.

Increasingly, buyers are acquiring properties not purely as investments, but as multi-generational family assets, designed to be used, enjoyed and held over time. This trend is particularly evident in established lifestyle destinations such as Marbella, where properties serve both as second homes and as long-term bases for international families.

This evolution reinforces demand for:

prime locations

turnkey properties

high-quality, low-maintenance homes

secure, well-established residential environments

What this means

The global positioning of Marbella strengthens the underlying fundamentals of the Costa del Sol property market.

International demand remains structurally strong

The market continues to attract globally mobile capital

Prime assets benefit from both scarcity and international relevance

Lifestyle-driven demand supports long-term value

At the same time, this global context helps explain the current phase of the local market: strong fundamentals combined with increasing selectivity.

Relative values

How many square metres of prime property US$1m buys in selected cities.

Price per square metre in Marbella is for prime property in A+++ location.

Source: Knight Frank The Wealth Report 2026 / DM Properties

Key findings

What defines the current market cycle

The market rebounded in spectacular fashion after the initial Covid shock of 2020

Growth, though still impressive, has been slowing somewhat since the peak year in 2022

The same is true of price increases, though these vary from municipality to municipality

The market’s ability to absorb these price increases is reducing, especially in all but the upper segment

Sales in the Golden Triangle moderated slightly in 2025 (down approximately 4.5% compared with 2024), with early 2026 data pointing to a more selective but still active market.

Though the economic growth forecast for Spain in 2026 has been downgraded a little to 2,1% due to the geopolitical situation, it remains one of the fastest-growing economies in Europe

The Spanish economy is forecast to continue growing in 2026, at around 2.3% - 2.4%, still well above the EU and eurozone averages.

Periods of geopolitical uncertainty continue to support demand for safe, well-connected lifestyle markets such as the Costa del Sol, reinforcing the region's appeal to international buyers.

If this is not so there will be a reduced rate of growth to accompany a slowing in the increase of property prices

The greatest prospects for price growth driven by surplus of demand over supply are found in prime locations, but the greatest dynamism in the market is provided by newly upcoming areas that are attracting new attention from developers and buyers alike for the value for money and growth potential they offer.

In short, the data points to a market entering a more balanced phase. Transaction volumes are moderating after several exceptionally active years, while price growth is stabilising. demand remains solid, especially for prime and well-priced homes, with buyers becoming more selective.

Contributors and Research: Pia Arrieta: Principal Partner Mariano Beristain: Managing Partner Mar Poza: Marketing and Research Manager

Urban Planning content updated in June 2026 by Javier Pérez de Vargas, Lawyer Partner at Pérez de Vargas Abogados.